The Growth Story Behind Buy Now Pay Later

The meteoric rise of BNPL was driven by strong product market fit and viral growth loops in the product. Here's a break down.

Summary

The meteoric rise of Buy Now Pay Later has been largely driven by strong product market fit and viral growth loops in the product. Where BNPL innovated was selling to the CMO (vs. the CFO or CTO) and partnering closely with them. This allowed the payment method to be deeply integrated into the customer journey, leading to our two growth loops.

Here's what we cover

Introduction

Whatever your opinion of Buy Now Pay Later, it’s growth has been staggering.

From being the talk of the town with Affirm and Klarna touting massive valuations and AfterPay being acquired by Square (now, Block) for $29 billion in August 2021, there was a period of time where Buy Now Pay Later businesses were seemingly everywhere.

So what’s the secret sauce?

I would love to say that BNPL attracted the best founders and the best growth teams. But there’s a simpler explanation than that.

As a growth marketer at BNPL hoolah.co I saw that the secret sauce was the product itself: the BNPL product has inherent growth loops that help it:

- Thrive as a viral idea

- Create natural growth loops in merchant and consumer acquisition

Let’s dig more into this as well as the other success factors for Buy Now Pay Later.

👉🏼 Also, check out this deep-dive into AfterPay’s growth strategy by my friend David Fallarme which covers a number of other, fascinating growth levers.

Table stakes — BNPL (f**king) works

i.e. It’s 10x easier scaling a great product

Putting growth loops aside I saw the proof in the pudding as hoolah helped merchants knock it out of the park and grow their business by:

- Driving GMV

- Increase basket size

- Driving new consumer demographics to purchase

- A host of second order benefits for merchants, including connecting better with customers, reducing the need to discount, etc.

Having a great product and product-market fit is table stakes and makes driving the growth loops a whole lot easier.

Great product ➡️ High NPS ➡️ Lower CAC & Churn

The stroke of genius — selling payments to the CMO

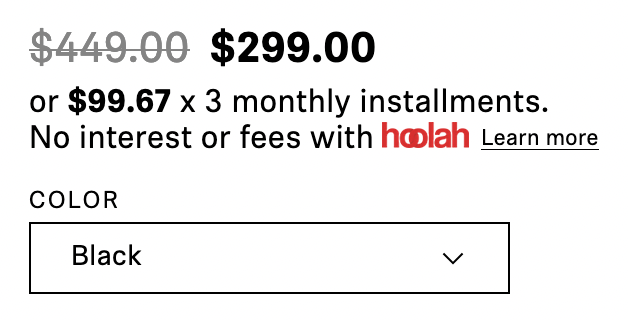

A key innovation that BNPL brought was selling a payment method to the CMO.

Where most payments companies were selling to the CFO or the CTO, BNPL tailored their value proposition towards the CMO by speaking about driving visitors, improving conversion and average order value.

With the marketing team’s support they were able to integrate the BNPL proposition into the entire customer journey, including the paid ads, Instagram posts and stories, check out page, abandoned cart emails, and newsletters.

This explains why BNPL was seemingly everywhere you looked with what turns out to be very little financial investment required. This “wall of content” spawned two growth loops which propelled BNPL further.

Growth Loop #1: Merchants beget Merchants

The BNPL sales and customer success cycles was straightforward:

- Sales: Sell to the CMO

- Success: Activate Merchants by integrating BNPL into their acquisition channels

- Repeat.

“Activating Merchants” became really important to spin the first growth loop.

Because most retailers follow their competition closely, when a single retailer launched publicly with a BNPL platform, this would alert all of their close competitors. Curious competitors would find out more and often find themselves enticed to add BNPL to their stores.

Newly Activated Merchants ➡️ Merchant Awareness ➡️ New Merchants ➡️ Newly Activated Merchants… and so on.

Growth Loop #2: Merchants beget Consumers

What we discovered early on at hoolah.co was that the BNPL proposition will eventually makes sense to the consumer for the right brand and the right product.

For example:

- I see BNPL at the bookstore. I ignore it.

- I see BNPL, again, at Secretlab. I ignore it.

- I see BNPL for a pair of Nike trainers I’ve been eyeing for a few weeks. The value proposition clicks ✨ aka the “aha moment”

It’s hard to predict and control when the customer experiences the “aha moment”, but here’s what you can control — getting the payment option in front of more customers and more often.

Again, activating merchants is the critical piece. Activating merchants gets BNPL in front of more consumers and thereby generates more transactions.

Newly Activated Merchants ➡️ Consumer Awareness ➡️ Transactions

By putting the two growth loops together, BNPL businesses needed to focus on activating merchants and this would drive both new consumer transactions and new merchant leads.

This powerful growth loop lead to exponential growth for many BNPL businesses. Furthermore, a single merchant can be “activated” several times, allowing you to spin this growth loop faster and faster.

A better credit product, re-imagined for millennials

BNPL made credit accessible to millennials. This made a lot of people upset — they felt that BNPL succeeded by giving credit to a group of people that traditional institutions (i.e. cards) would not touch.

Not only do I think that’s not true, but that would also be selling BNPL short.

BNPL built a great consumer experience that out-rivaled the credit card experience. Here’s what BNPLs generally did well:

- The “app” experience — BNPLs were deeply integrated into the point of sale allowing you to see exactly what you bought and from which retailer. The apps provided a great experience (it’s funny this even needs to be mentioned) and gave consumers a lot of control over their credit.

- Easy to use — No minimum spend, card agnostic (works with any debit or credit card), and you get approved in seconds. This does wonders for experience (and also thereby, conversion).

- Less shady behaviour — The leading BNPLs want you to pay on time and not accumulate late payment fees, so they incentivise timely payments (for example, Affirm makes no money from late payment penalties). Compare this to credit cards who will slap a penalty fee as soon as they can and where penalty fees account for significant revenue.

- On brand — without the corporate shackles, BNPLs were a whole lot more in tune with their target audience.

A wide Total Addressable Market

Sales rep: Do you sell direct-to-consumer?

Customer: Yes

Sales rep: Well then you should consider Buy Now Pay Later.

It certainly helps that BNPL works for almost any retailer, whether they sell online or offline. This means:

- You can grow bigger as a business

- You can pitch far and wide

- You turn away fewer people

Coming from a B2B SaaS background, it blew my mind how much wider the TAM was and how much it easier this made it to sell 🤯

Headwinds and the future of BNPL

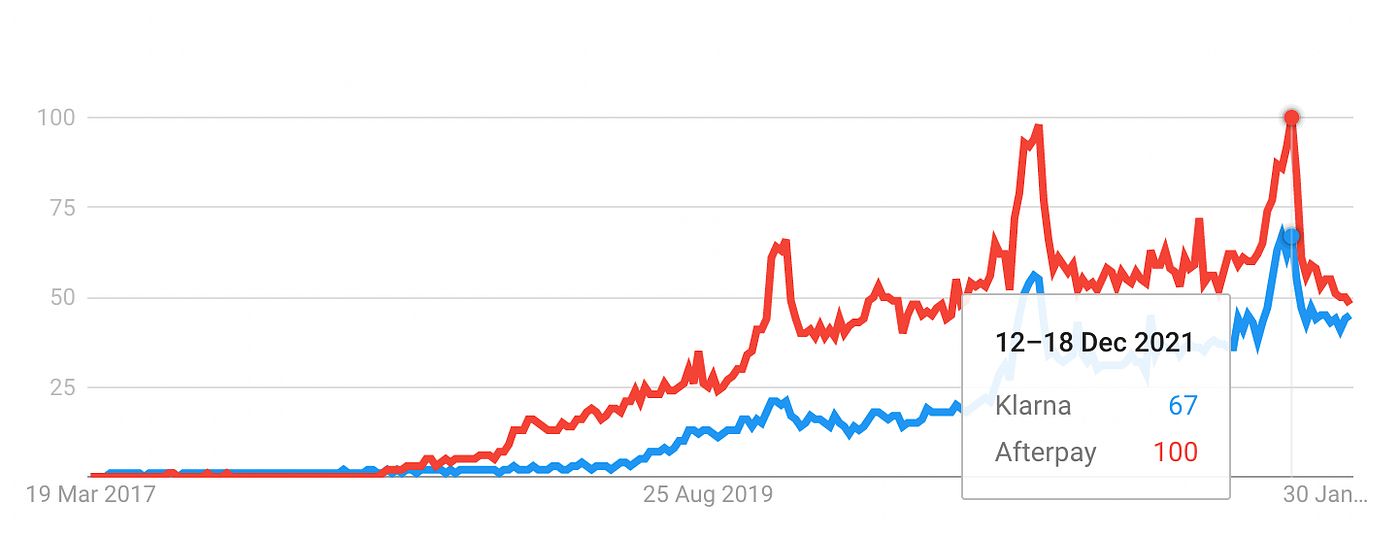

If you look at the trends chart at the start of this post, you can see that BNPL’s star is arguably waning. The sharks are out with many fintech professionals calling out BNPL as a one-hit wonder or as a “payments feature” and not a complete product on its own.

Looking closer, it’s clear that in many ways BNPL has become a victim of its own success.

Because of the strong, inherent growth loops in BNPL there is a strong disincentive to lose a deal to a competitor. Pair this with VC pressure to grow and rising competition, BNPLs faced a tight squeeze on margins really quickly. It wasn’t uncommon to see BNPLs selling below cost or promising outsized marketing budgets to lure merchants away from the competition.

The rising cost of borrowing and increase in regulatory scrutiny will also increase costs in the medium term.

With profits on the decline and costs increasing, this will likely be unsustainable in the long run and the consolidation is underway.

All said and done, BNPL did rock the tech (not just fintech) space, and did many things right. The leaps forward by BNPL in consumer experience and a better integrated value proposition is here to stay. Consumers have experienced something a lot better than what they got with credit cards, and card companies will need to quickly catch up.

Thanks for reading this far!

In the lead up to this post there were questions from my network around the efficacy of BNPL, adoption across markets, and so on. It was tough for me to cover that in this post, and I’ve tried to share as much feedback as possible directly (and in some cases via DMs). Safe to say, I feel that BNPL has strong-product market fit across most retail industries and in most countries.

Also, this is a post that I’ve been wanting to write for a long time. It coalesces a fair bit of my learnings and reflections on growth in BNPL.

If you have questions or are curious to learn more, feel free to hit me up on LinkedIn or Twitter. 👋

You can also follow me or hit subscribe to keep in touch. I write regularly about growth, marketing, and partnerships in tech and fintech.